Which Retirement Plan Lets Entrepreneurs Stockpile Millions?

SEP, SIMPLE, and Solo 401(k) comparison for reducing taxes and retiring rich

Quick Take—Why This Matters

You didn’t quit the 9-to-5 grind to hand your hard-earned revenue back to the IRS. The right retirement plan lets you shelter six figures of income today and harness tax-deferred (or tax-free) growth for decades. Pick the wrong plan and you’ll still retire, just with a lot less freedom.

Ready to steer clear of costly mistakes and unlock next-level insights? Subscribe to our premium newsletter for exclusive strategies, in-depth analysis, and expert-only content designed specifically for high-achieving entrepreneurs.

Why 2025 Is a Pivotal Upgrade Year

Picture the U.S. tax code as a constantly moving goalpost. In 2025, that goalpost leapt forward thanks to SECURE 2.0’s inflation indexing, bigger catch-ups, and new Roth mandates. Here’s what changed and why entrepreneurs should care:

Higher ceilings, same effort.

The Section 415(c) cap jumped to $70,000, meaning your existing contribution formula can shelter more dollars than last year without lifting a finger.“Super” catch-ups for the pre-Medicare crowd.

Individuals aged 60–63 now receive an additional $11,250 (or $5,250 within a SIMPLE). If you’re in that window, you just won the tax lottery—use it.Roth catch-up mandate on the horizon.

Starting in 2026, anyone earning $145,000 or more in FICA wages must funnel catch-ups into a Roth IRA. Flip the switch now and test-drive your future tax-free bucket while the market is still giving you a multi-year runway.Inflation adjustment on SIMPLE and SEP.

SIMPLE salary-deferral rose to $16,500; SEP’s percentage-of-pay formula now maxes at $ 70k—a clean, round number that makes quarterly tax-estimate math easier than ever.Plan startup credits worth up to $ 15k.

New or micro-employers (≤ 100 workers) can wipe out most, if not all, of their plan setup costs. Translation: you’re getting paid to stop procrastinating.The asset threshold for the 5500-EZ didn’t budge.

The filing trigger is still $ 250k. Thanks to the beefed-up limits, you’ll hit that faster—budget the admin time now instead of paying $250/day penalties later.

Bottom line: 2025 isn’t “just another year.” It’s a bigger sluice gate for sheltering income, and the water (your cash flow) is rising. Open the gate.

2025 Side-By-Side Showdown

*Assumes a 3% employer match on a $100,000 salary.*

Read between the rows

Solo 401(k) is the heavyweight. It layers employer profit-sharing on top of employee deferrals, offers Roth flexibility, and unlocks monster catch-ups at 60–63.

SEP IRA is the gentle giant. High limit, zero paperwork, but no salary deferral or catch-up turbo boost.

SIMPLE IRA is the Swiss Army knife. Light admin, mandatory match keeps employees happy, yet its ceiling is barely a third of a Solo 401(k).

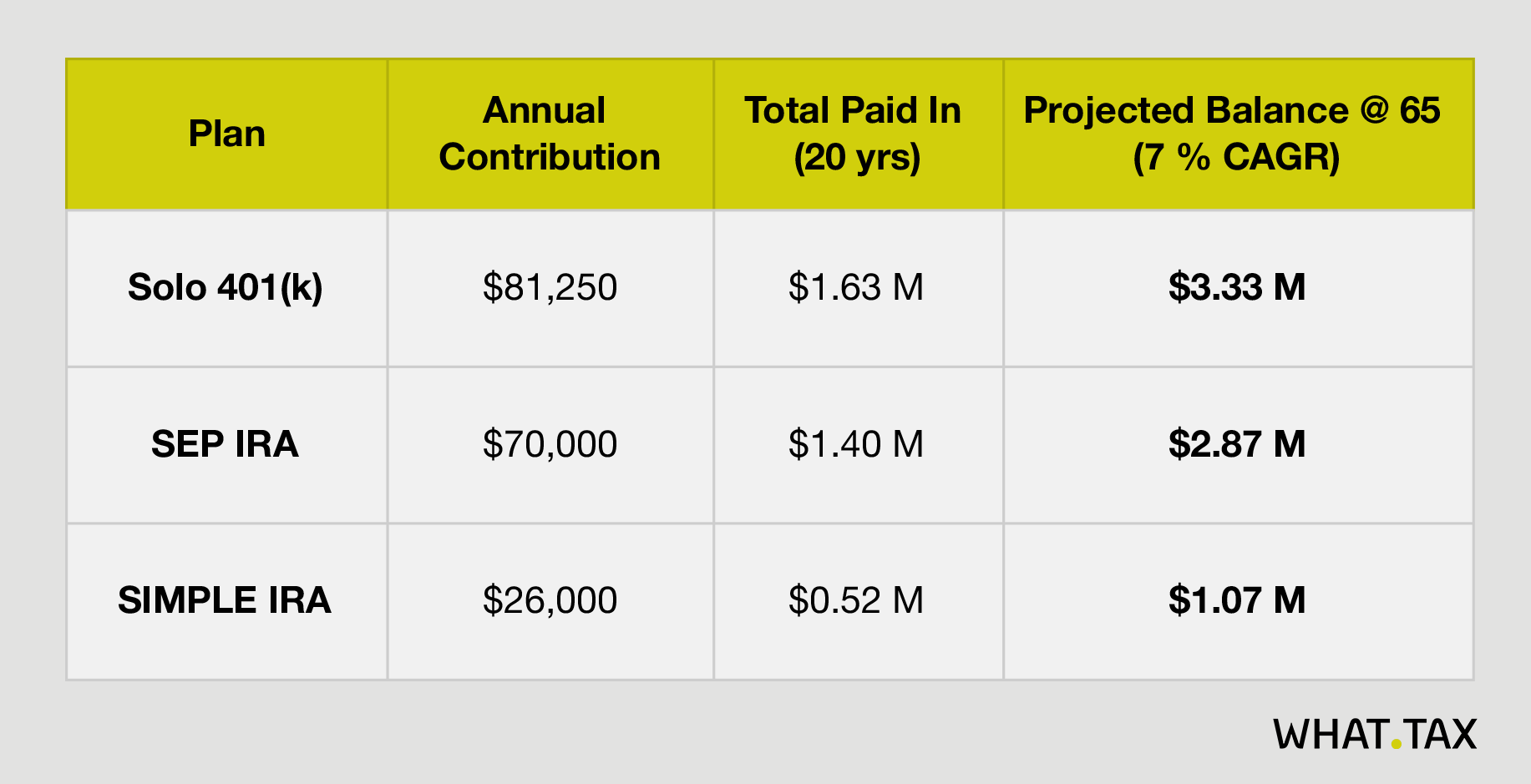

Case Study—20 Years of Compounding on a $ 300k Net

Even before taxes, the Solo 401(k) finishes $2.26 million ahead of the SIMPLE, enough to buy two beach houses or fund 25 years of $ 90k retirement spending.

Tactical Edge—How to Squeeze Every Dollar

Below is a stronger, field-tested playbook you can drop straight into the article.

1. Front-Load Contributions on January 2nd

Every $10 K dropped into a tax-sheltered account on Day 1 instead of December 31st buys you an extra year of compounding—roughly $19 K more after 20 years at 7 %. Automate ACH drafts from your business checking the moment quarterly cash clears so momentum, not memory, funds your future.

2. Exploit the New “Super Catch-Up” Window (Ages 60-63)

SECURE 2.0 allows individuals aged 60, 61, 62, and 63 to contribute an additional $11,250 to 401(k) plans (or $5,250 to SIMPLE IRAs) on top of the standard $7,500 catch-up contribution, thereby increasing the employee deferral to $34,750 in a Solo 401(k). This is a $ 45,000 tax deduction (or Roth stash) that disappears once you reach 64—set a calendar reminder now.

3. Turn After-Tax Dollars Into a Mega Backdoor Roth

If your Solo 401(k) document permits after-tax (non-Roth) employee contributions, you can:

Max the regular limits (pre-tax and/or Roth to $23,500 + catch-ups).

Contribute after-tax up to the $70 K 415(c) ceiling (or $81,250 with super catch-up).

Immediately convert those after-tax funds to the plan’s Roth sub-account or out to a Roth IRA.

Result: up to $81,250/year, all growing tax-free—no income cap, no pro-rata rule.