Three Tax-Optimized Business Models for 2025 Scale

Deep-Dive Playbook for U.S. Founders to Slash Taxes, Compound Cash Flow, and Outsmart the 2026 Policy Cliff

A quick mental picture

Imagine you’re on the grid at the Miami F1 Grand Prix. Two identical cars sit revving—but one has the DRS flap jammed shut while the other gets a full aerodynamic boost down every straight. Both drivers are brilliant; only one has engineered an advantage so significant that talent alone can’t close the gap. That’s the difference strategic tax planning makes to identical businesses in 2025.

The U.S. tax code offers more horsepower than ever—if you pick the right vehicle:

Subscriptions for dependable cash flow and depreciation windfalls.

Licensing for royalty income that’s taxed at a discount.

Hybrid structures that cherry-pick the best incentives from C-Corps and pass-throughs.

Ready to steer clear of costly mistakes and unlock next-level insights? Subscribe to our premium newsletter for exclusive strategies, in-depth analysis, and expert-only content designed specifically for high-achieving entrepreneurs.

Below is your actionable playbook—lean on jargon, heavy on numbers, and trimmed to two tables you can screenshot and revisit at tax time.

1. Subscription-Based Models — The Recurring-Revenue Tax Magnet

1.1 Why the IRS loves your subscription—but lets you keep the cash anyway

Predictable recurring revenue gives the IRS confidence you’ll be around to pay next year, so Congress rewards you with front-loaded deductions that juice your current-year cash flow:

40 % bonus depreciation (2025 only). Anything with a valuable life of ≤ 20 years, such as servers, edge devices, and network racks, can be expensed upfront instead of over five years. A $ 400k GPU cluster placed in service on December 31, 2025, creates a $ 160k deduction the same day you plug it in.

§179 expensing—now $1.25 M. After bonus depreciation, elect §179 on the remaining basis. The phase-out doesn’t start until $3.13 M, so most SaaS and membership sites can still take the full hit.

R&D payroll credit (up to $ 500k). Unlike the “regular” R&D credit, this one offsets the FICA/Medicare tax you already remit. Every $1 of credit equals $1 less cash leaving the bank on payroll day.

Cash-method accounting up to $30 M gross receipts. Sub-$30 M businesses can stick with a cash basis, meaning the annual spike of prepaid subscriptions (Black Friday deals, lifetime plans, etc.) isn’t taxed until you deliver the service.

1.2 Stacking the incentives — an illustrative year 1 walkthrough

January: You form an LLC taxed as an S-Corp. Founders set a “reasonable compensation” at $ 120,000 each; excess profit flows out free of the 15.3% self-employment tax.

March: Sign a $ 450k purchase order for H100 GPUs. You place them in service by June, triggering $ 180k bonus depreciation.

June–September: Hire four W-2 engineers at $ 140k each to build proprietary recommender models. Qualifying wages (~$ 560k) generate the full $ 500k payroll credit, wiping out eight months of federal payroll taxes across the whole staff.

Year-end: Gross subscription receipts hit $4.2 M; deferred revenue (annual plans) is $1.4 M, but on a cash basis, you’ve recognized only $2.8 M. After deductions, taxable income shrinks to nearly zero while free cash flow tops $1 M.

1.3 Advanced levers most founders overlook

Cost segregation for data centers. If you lease colocation space, a qualified study can reclassify electrical, HVAC, and raised-floor components into 5- or 7-year property, multiplying the assets eligible for bonus depreciation.

Software capitalization pivot. Section 174 now forces amortization of internal-use software over five years, but if your dev work aims at a new, externally licensed module, you may treat costs as §197 intangibles and take a one-time §197 disposition deduction when you sunset the module.

State-level R&D piggybacks. Thirteen states (including CA, CO, and TX) mirror the federal credit; stacking them allows you to reclaim up to an additional 6–8% of qualified wages.

Deferred revenue financing. Banks will lend 30–40 % of ARR at SOFR + 300 bp, but the interest is fully deductible, letting you arbitrage tax savings against growth investments.

1.4 Red-flag mistakes that trigger audits

No W-2 wages in an S-Corp. The IRS auto-flags K-1 distributions with zero payroll. Utilize industry surveys, such as Payscale and Robert Half, to justify the salary split.

Claiming bonus depreciation on used servers from your prior LLC. Related-party purchases fail the “original use” test; instead, leave them in the old entity or elect §179 (if cap room remains).

Capitalizing all software costs under §174 by default. First, identify which features are R&D vs routine maintenance; only the former must be capitalized.

Miscalculating the payroll credit. Only qualified wages count—exclude 1099 contractors and any employee who owns > 5 % of the company.

1.5 Key takeaways for 2025 action items

Buy or lease hard assets this year—40 % bonus drops to 20 % on 1 Jan 2026.

Max out the $ 500k payroll credit before headcount balloons and you switch to contractor-heavy staffing.

Lock in S-Corp status now to harvest one more year of the 20 % QBI deduction.

Document everything (board minutes, POs, time-tracking). The bigger your write-offs, the more pristine your paper trail must be.

Play these cards right, and your subscription engine becomes a self-funding growth flywheel—one where the IRS essentially foots the bill for your next feature release.

2. Licensing Models — Royalty Income at a Discount

The IRS treats royalties as “income from the use of property,” not earned income from your labor. That single distinction unlocks lower headline rates, generous cost recovery, and a buffet of cross-border arbitrage opportunities.

2.1 Why royalties get the velvet-rope treatment

20 % QBI deduction (IRC §199A) — still alive through December 31, 2025. If your licensing LLC has $1 million of domestic royalty income, only $ 800k is taxed.

FDII deduction (IRC §250) — a U.S. C-Corp that licenses IP abroad can whittle its federal rate to 13.125 % on that foreign royalty stream.

Treaty-reduced withholding — more than 60 countries cap U.S. royalty withholding at 0–5 % (e.g., Netherlands 0 %, U.K. 0 %, France 0–2 %). Stack that with FDII, and your global effective rate can slide below 15%.

Amortization & basis step-ups — acquired IP is amortized over 15 years (§197). But every time you sell or gift the IP, the buyer gets a fresh 15-year clock—handy when you want to “refresh” deductions without spending new cash.

2.2 Architecture of a modern licensing stack

Step 1 — Separate creation from ownership

DevCo (S-Corp or partnership) builds the software, designs, or content, and collects R&D credits.

IP HoldCo (U.S. C-Corp or foreign DAC) acquires the IP at fair market value and becomes the licensor.

Step 2 — Route royalties intelligently

U.S. customers pay royalties to HoldCo, → qualifies for QBI.

Non-U.S. customers pay the same HoldCo → qualifies for FDII.

If you prefer a pass-through, license IP to an LLC taxed as a partnership, and let the royalty flows keep QBI status.

Step 3 — Cash-out options

Charitable Remainder Trust (CRT) — donate mature IP, license it back, and receive a 5 % annuity for life while deferring capital gains.

QSBS play — contribute the IP to a brand-new C-Corp and hold for five years; up to $10 million of gain can be 0 % at exit.

2.3 Illustrative Year-1 walkthrough

April 2025 — Creator forms Sunrise IP, Inc. (C-Corp). DevCo sells a voice-cloning model for $2 million (arm 's-length price). Sunrise books §197 intangibles and starts a 15-year amortization: $ 133k deduction per year.

May 2025 — Sunrise licenses the model back to DevCo for 10 % of revenue, payable monthly.

June–December 2025 — DevCo sells $4 million in API calls; pays Sunrise $ 400k royalties. DevCo claims the 20 % QBI haircut. Sunrise claims FDII on $ 250,000 of royalties from EU customers, reducing its corporate bill to ~13%.

Tax season 2026 — Combined federal outflow: ≈$ 88k on $4 million in gross revenue (about 2.2 % effective) before state offsets.

2.4 Advanced levers most founders leave on the table

Cost-sharing arrangements (CSA). Shift future IP value to a low-tax subsidiary (e.g., Ireland 12.5 %) by having that entity “co-develop” new features in exchange for a buy-in payment. Done right, 80% + of future foreign profits escape U.S. tax.

IP Box migrations. Countries like the U.K. and Switzerland offer 10 %–12 % “IP box” rates on qualifying royalties. A treaty-friendly outbound transfer (Sections 367 & 482 compliant) can lock those rates for a decade.

High/low-tier royalty stacking. Charge a low-rate platform fee and a high-rate premium feature fee, so that the bulk of the profit runs through the most favorable regime.

“Use it or lose it” §174 planning. Development costs that create new intellectual property (IP) must be capitalized over five years, but expenditures for maintenance and bug fixes are still deductible. Careful time-tracking can result in significant six-figure deductions.

2.5 Audit magnets and how to defuse them

Royalty rate pulled out of thin air. Use third-party comps (RoyaltyStat, ktMINE) or an income method valuation to justify 5 % vs 15 %.

All offshore substance, no staff. A zero-employee Cayman HoldCo licensing $5 million of code invites a §482 “income re-allocation.” Park at least R&D or legal functions where the IP legally resides.

FDII without documentation. Please ensure the end-user is located outside the U.S. Maintain geo-IP logs, invoice addresses, or distributor attestations.

Treating personal-service income as royalties. If you show up on-site and train clients, the IRS will reclassify part of that “royalty” as fee-for-service, taxed at ordinary rates and subject to SE tax.

2.6 2025 To-do list (Licensing edition)

Set fair-market royalty rates now; valuations get harder if interest rates fall and multiples expand.

File a protective FDII election with your first C-Corp return—late elections are nearly impossible.

Finish any outbound IP transfers by 12-31-25 while the 13.125 % FDII rate still offsets GILTI exposure.

Pre-pay legal for CRT or QSBS restructuring so the five-year or annuity clocks start ticking before bonus depreciation drops to 20 %.

Master these moves and royalties morph from “nice side income” into a reliable, low-tax cash geyser—fuel you can redeploy into the next subscription or hybrid venture without ceding an extra lap to the IRS.

3. Hybrid Models — The Asset-Light Empire

A hybrid stack lets you bolt together the best incentives of C-Corps, S-Corps, partnerships, and territorial regimes—without schlepping around a bloated org chart. Think Lego®, not Jenga®: each block has one job, clicks neatly into place, and can be swapped out if Congress rewrites the rules.

3.1 Why bother mixing entities?

R&D today, cheap equity tomorrow. A C-Corp earns unlimited R&D credits at a flat 21 %, then exits at 0 % capital gains after five years under QSBS (§1202).

Immediate cash to founders. An S-Corp sales arm passes profit through the 20 % QBI deduction—and avoids the 15.3 % self-employment tax on anything above “reasonable comp.”

Location arbitrage. A Puerto Rico Act 60 subsidiary bills mainland customers at a 4% corporate tax rate—dividends are then sent back to the U.S. tax-free.

Liability firewall. If the sales arm gets sued, the C-Corp still owns the crown-jewel IP. If VC investors join the C-Corp, they never have to deal with the K-1 chaos of the operating LLC.

3.2 Blueprint: six moving parts, one tight loop

HoldCo LLC (partnership)

Members: founders + optional friends-and-family investors

Job: own everything; issue a single K-1; step-up basis at exitIP DevCo (Delaware C-Corp)

Job: hold patents/code; employ engineers; bank R&D credits; start QSBS clockSalesCo (S-Corp or partnership)

Job: sign customer contracts; pay founders W-2 salaries; distribute margin via K-1Puerto Rico Op-Co (4 % Act 60)

Job: support/fulfillment; invoice SalesCo; keep margin offshore until neededRoyalty Bridge Agreement

SalesCo → C-Corp: 8 – 12 % arm’s-length royalty on U.S. revenue (QBI eligible)

SalesCo → PR Op-Co: cost-plus-10 % for services rendered in Puerto RicoSolar/EV SPV (LLC disregarded to C-Corp)

Job: install rooftop solar + buy electric delivery vans; claim 30 % energy credit + 40 % bonus depreciation while leasing assets back to SalesCo

Cash flow: Customer ➜ SalesCo ➜ royalties/service fees ➜ C-Corp & PR Op-Co ➜ dividends/loan backs ➜ HoldCo ➜ founders.

3.3 Walk-through: Year 1 numbers

June 2025 – C-Corp books $900k qualified R&D wages, netting $90k federal credit (10 % rate) and state piggybacks worth another $25k.

July 2025 – SalesCo closes $3m in ARR, paying the C-Corp a 10% royalty of $ 300k. After §199A, only $240k is taxed.

August 2025 – Solar SPV installs a $400k array: $120k IRA credit + $160k bonus depreciation = $280k shelter in year one.

December 2025 – PR Op-Co earns $ 600,000 in support fees, taxed at 4% ($ 24,000). Dividend returns to HoldCo tax-free; founders borrow against basis at < 4 % interest—cash in pocket, no current tax.

Effective combined federal rate: ≈ 11 % before personal brackets.

3.4 Advanced levers to juice the model

ESOP Exit: Sell up to 100 % of the C-Corp to an ESOP, defer—or permanently avoid—capital gains, while the company deducts purchase-price principal.

Shareholder loans vs. dividends: Loans from HoldCo to founders create immediate liquidity without triggering dividend tax; interest paid back is deductible to the borrower entity under §163(j) limits.

Up-C conversion: When IPO time arrives, merge the LLC into a C-Corp and issue “exchangeable units”; the built-in gain generates a basis step-up that public investors pay you for via a TRA (tax receivable agreement).

State tax arbitrage: Plant SalesCo in Wyoming or South Dakota (0 % corporate/individual tax) while keeping C-Corp R&D staff in a credit-heavy state like Texas or Colorado.

3.5 Hidden trip-wires (ignore at your peril)

Transfer-pricing mismatch. A royalty above 25 % of SalesCo's revenue will scream “not arm’s-length” to the IRS. Stick to market studies or the comparable profits method.

Act 60 presence test. At least one C-level exec or a 4-person management team must be bona fide Puerto Rico residents; calendar-day counts matter.

QSBS bust-ups. Don’t buy back shares or pay out > 10 % of assets in cash within two years—both can disqualify the C-Corp’s stock.

Earnings stripping (§163(j)). Too much intercompany debt and your interest deductions get capped at 30 % of “adjusted taxable income.” Maintain a debt-to-equity ratio of approximately 1:1 and document the terms.

3.6 A 90-day sprint to lock benefits before 2026

Weeks 1-2: Form entities; sign intercompany agreements; open separate bank accounts.

Weeks 3-6: Move IP into C-Corp at FMV; file §83(b) on founder stock; start QSBS clock.

Weeks 7-10: Order solar/EV assets so they’re placed in service by Dec 31, 2025—critical for 40 % bonus depreciation.

Weeks 11-13: Elect S-Corp status (Form 2553) effective Jan 1, 2025, if not already done; update payroll so founders take reasonable comp.

Year-end: File R&D Form 6765, energy credit Form 3468, and Puerto Rico Act 60 compliance package. Archive transfer-pricing report.

Bottom line: A lean hybrid stack is a Swiss Army knife: cut your effective tax rate, raise VC-friendly equity, siphon cash to founders, and preserve a clean exit—all while staying light enough to pivot when the next tax bill drops. Build it once in 2025, and you’ll compound the advantage for years.

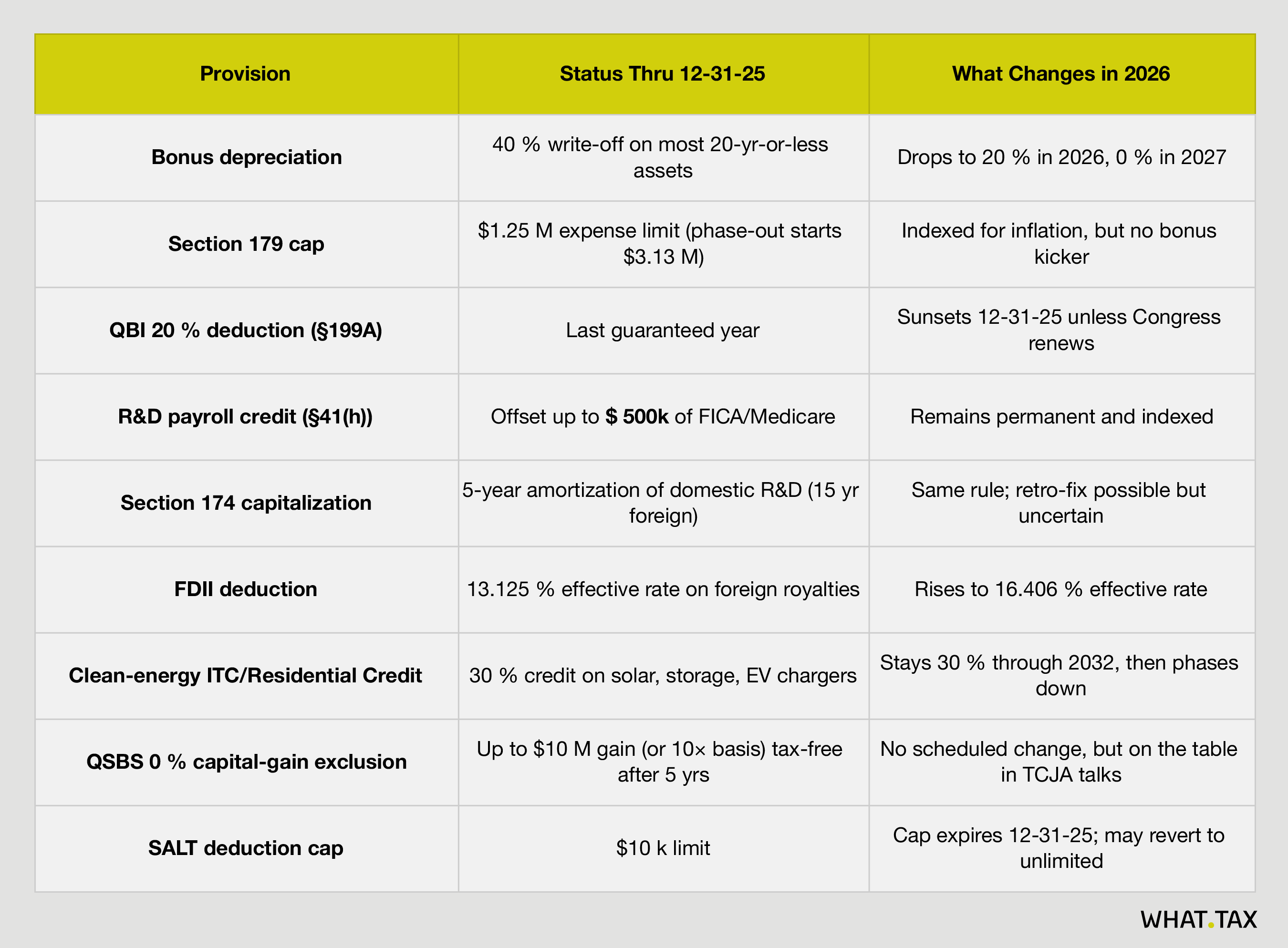

2025 Deadline Cheat Sheet

What do these dates mean for founders right now?

Lock in hard-asset purchases before New Year’s Eve to capture the 40 % bonus + full §179.

Front-load pass-through profit and finish entity conversions in 2025—the QBI haircut may vanish in 2026.

Document R&D rigorously so you can claim both the §41 payroll credit and defend five-year §174 amortization if Congress fails to repeal it.

Consider a C-Corp for foreign licensing while the 13.125 % FDII rate still beats the post-2025 16.4 %.

File Form 3468 (energy credit) or lock a solar/EV SPV into service this year; the 30 % credit is safe, but you want to combine it with the higher bonus depreciation rate.

Start the QSBS clock on any new C-Corp shares now—five years from today is spring 2030, comfortably before the potential tightening of the exclusion.

Treat these deadlines like closing bells on Wall Street: once they ring, the windows slam shut—or at least get a lot more expensive to reopen.

Avoid These Costly Pitfalls

Zero W-2 wages in an S-Corp → triggers a “reasonable compensation” audit. Benchmark salary at ~30–40 % of net profit or industry comps.

Bonus depreciation on used gear from related parties → disallowed; elect §179 or lease instead.

Treating foreign-source royalties as qualified business income (QBI) → fails. Route those through a C-Corp and claim FDII.

Puerto Rico Act 60 without real presence → IRS treats mainland work as U.S. source. Keep core management or coding physically on the island.

Bottom Line

The tax code is not a maze—it’s a menu. 2025 is the last full year that some of the tastiest items will remain:

Front-load capital purchases while 40% bonus depreciation pairs with a robust §179.

Squeeze every dollar of pass-through profit under the 20 % QBI umbrella.

Layer R&D, FDII, and clean-energy credits to push your effective rate toward the low teens.

Play it right and you’ll cross the seven-figure threshold with more cash on hand and an investor-worthy cap table.