The Million-Dollar Question—When to Shift from LLC to S-Corp or C-Corp?

Cracking the Code on Tax Structures to Unlock $50k+/Year in Savings

Hello, Dear Entrepreneur!

Today, we’re tackling the million-dollar question for growing businesses: when and why to pivot from an LLC to an S-Corp or C-Corp. With potential tax savings of $50k+ per year on the line—and the looming expiration of key TCJA provisions—this isn’t just a casual choice. In this newsletter, we’ll break down the critical factors (from self-employment tax strategies to reinvestment opportunities) and equip you with the knowledge to structure your enterprise like a true tax asset. Let’s dive in!

The Tax Crossroads: Pass-Through vs. Corporate Structures

Every high-level entrepreneur must eventually confront the decision: maintain a pass-through entity (LLC/Sole Proprietorship) or transition to a corporation (S-Corp/C-Corp). The outcome isn’t merely a filing choice—it’s a strategic move with potentially five- to six-figure annual tax implications.

Three primary factors drive the optimal choice:

Income Level

Growth/Reinvestment Goals

Self-Employment Tax Exposure

2025 Update: Certain Tax Cuts and Jobs Act (TCJA) provisions are set to expire. For top earners, individual tax rates may revert to 39.6%, while the corporate rate remains at 21%. This looming shift makes proactive tax planning paramount.

The S-Corp Sweet Spot: Minimizing Self-Employment Tax

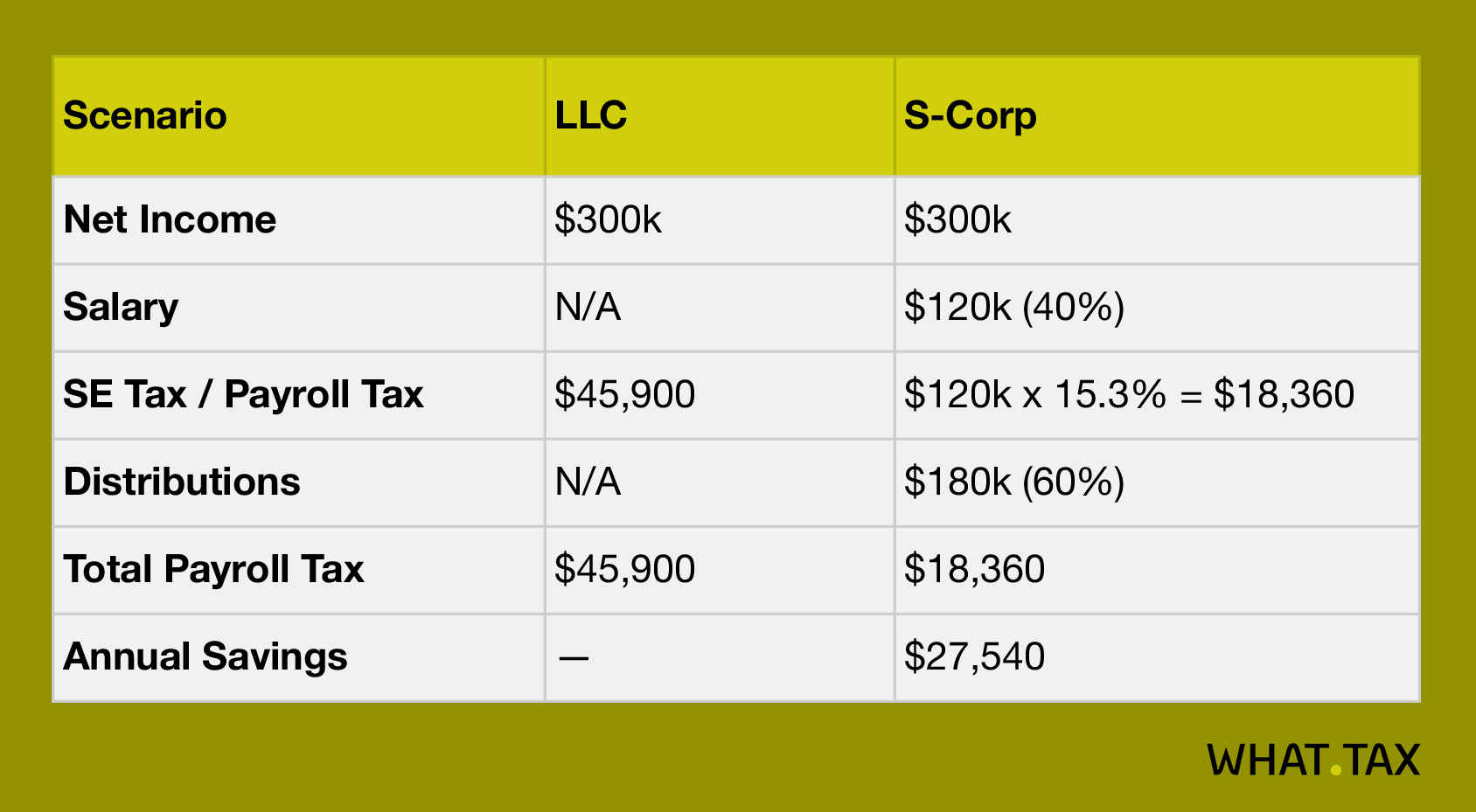

When an LLC’s net earnings start to exceed $45k-$50k, an S-Corporation election often emerges as the most immediate tax-saving lever.

Key Stat

LLC owners pay 15.3% self-employment tax on all net income.

S-Corp owners pay it only on the portion classified as salary, while distributions are exempt.

Illustrative Example

60/40 Rule (2025-Optimized)

Allocate roughly 40% of net income to “reasonable compensation” (subject to payroll tax), and the remaining 60% as distributions (exempt from payroll tax).