Tax-Efficient Investing Strategies to Help You Keep More of Your Returns

A 2025 Playbook for Entrepreneurs to hold longer, harvest smarter, and park every asset in its most tax-advantaged home

🚀 Why 2025 Is a Once-in-a-Generation Window

Think of 2025 as the last cheap ticket on a tax train that’s about to leave the station—and the conductor just announced, “Final boarding!” Here’s what makes the next seven months uniquely powerful for entrepreneurs and investors:

1. Tax rates are at their floor, and the elevator is heading up

Under today’s TCJA brackets, the top ordinary-income rate is 37 %. If Congress does nothing, the rate reverts to 39.6% on January 1, 2026, and every bracket below it also increases. (Tax Foundation)

Long-term capital gains, currently capped at 23.8 %, are projected to drift toward 25 %+ once the sunset hits, eroding the very advantage of “patient” investing. (The Tax Adviser)

A founder selling a $5 million stake after 12 months could owe $ 230k more in federal tax simply by closing the deal in January 2026 instead of December 2025.

2. You’ll never again have this much estate-transfer “headroom”

The federal estate-tax exemption is inflation-adjusted up to $13.99 million per person in 2025 (nearly $28 million for married couples). (Kiplinger)

On New Year’s Day 2026, it’s scheduled to shrink by roughly half, dropping to about $7 million (single) after inflation adjustments. That single change could expose an additional $6.9 million of family wealth to a flat 40% estate tax.

Failing to act could result in a $2.76 million tax bill on assets that would have been tax-free in 2025.

3. The gift that really does stop giving

For 2025, you can gift $19,000 per recipient (or $38,000 per child if spouses “split” gifts) without touching your lifetime exemption. (Investopedia)

Any unused annual gifting capacity evaporates at midnight on December 31, and gifts made after the sunset consume far scarcer lifetime exemption.

4. A fleeting chance to “stuff” ultra-high-growth assets into Roths & HSAs

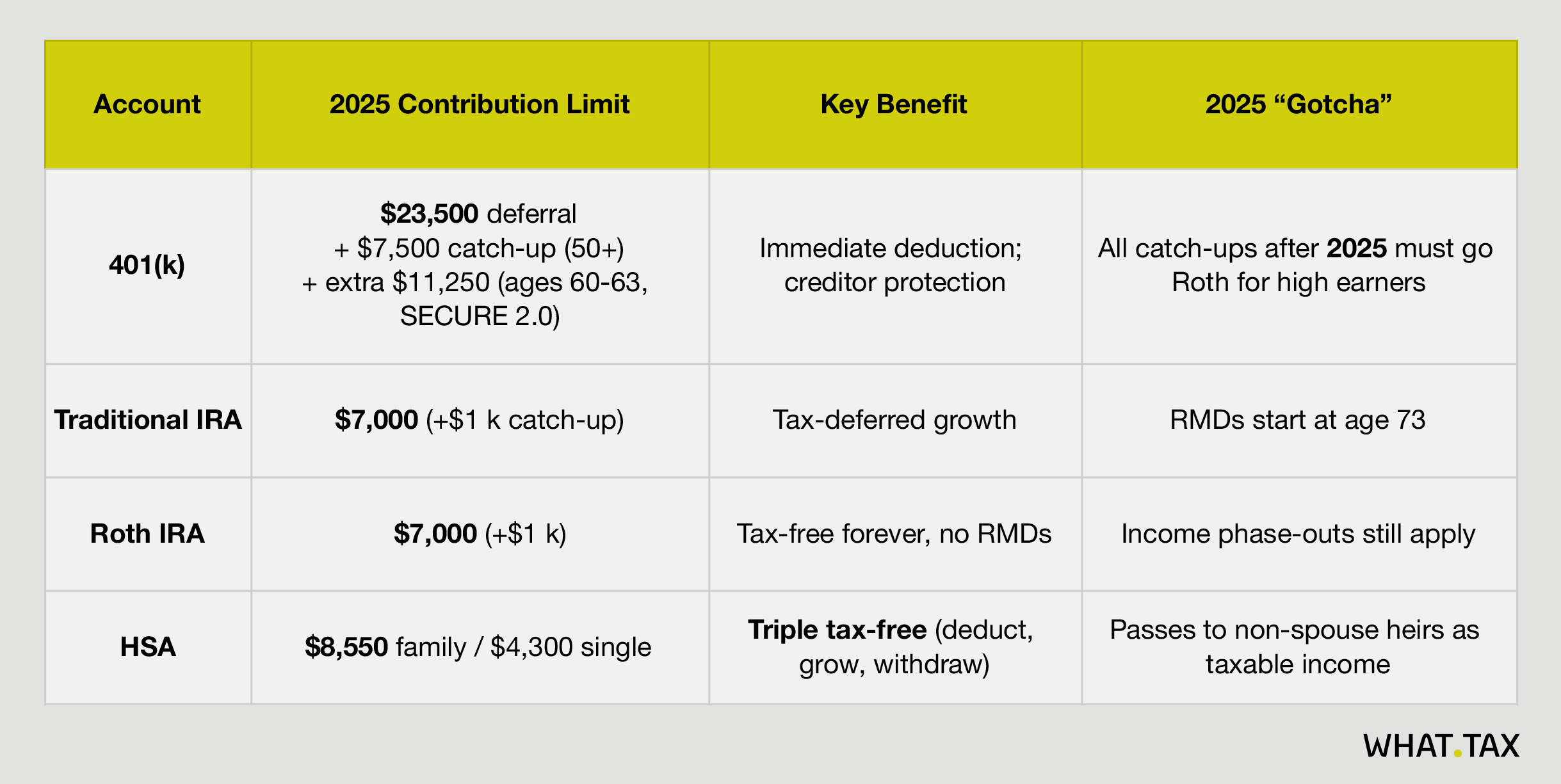

Contribution ceilings are marching higher with inflation—$23,500 for 401(k) deferrals, $7,000 for IRAs, $8,550 for family HSAs in 2025—yet the tax cost of future withdrawals (or Roth conversions) is poised to rise with the brackets. Locking in Roth space now is like pre-paying tax with a coupon that soon expires.

5. Legislative wildcards tilt the risk-reward toward acting early

Competing bills in Congress aim to either extend today’s rules or accelerate new, revenue-raising brackets. Betting on a favorable extension is a coin flip; acting in 2025 is guaranteed leverage on rules you already know. (Bipartisan Policy Center)

🎯 What This Means for You—In One Sentence

Every dollar you shift, harvest, convert, or gift before December 31 can grow for decades under a friendlier rulebook that may vanish overnight.

⚡ Ready for the deep-dive tactics that turn this window into a permanent advantage? Upgrade to Premium

🏛️ The Three Pillars of Tax Efficiency

Pillar A — Account Selection: Max Every Bucket

Reality check: Invest $10,000 in a Roth IRA vs. a taxable brokerage at 7% for 30 years—even with the current 23.8% capital gains rate, the Roth ends at $117,000 vs. $81,000. That’s a 44 % haircut purely from taxes.

Pillar B — Asset Location: Put Each Asset Where the IRS Hurts Least

Taxable account (low-drag):

Broad-market index ETFs

Municipal bonds (federal tax-free)

Positions you plan to tax-loss harvest

Tax-deferred account (IRA / 401 k):

High-yield corporate bonds (ordinary income)

REIT funds

High-turnover trading strategies

Roth or HSA (tax-exempt):

Highest-growth bets—small-cap value, AI disruptors, venture funds

Anything you want, compounding tax-free for decades

Pillar C — Holding-Period Management

Short-term gains (< 12 months): up to 40.8 % federal + NIIT.

Long-term gains (> 12 months): currently 23.8 %, but could rise in 2026—lock in lower rates now.

Entrepreneur tip: If you’re planning an exit, structure vesting and option exercises to clear the 12-month line before sale.