Solo 401(k) vs. SEP IRA: Which One Gives You the Biggest Tax Break?

A Side-by-Side Look at Contribution Limits, Administrative Costs, and Flexibility

Hello Smart Entrepreneurs!

Welcome back to the newsletter, where we break down powerful tax-saving strategies to help you keep more of your hard-earned money. If you're self-employed, you already know that saving for retirement isn't as straightforward as it is for traditional employees. But the good news? You have access to some of the most powerful retirement accounts out there—the Solo 401(k) and SEP IRA.

In today’s deep dive, we’re going to explore:

Which plan allows you to contribute the most (and at lower incomes)?

How to use Roth strategies to build tax-free wealth

The best option for business owners with a spouse

Which plan is easier to set up and maintain

By the end of this guide, you’ll know exactly which plan is the best fit for your business and financial goals—and how to maximize your retirement savings while legally reducing your tax bill. So, let’s jump right in!

Choosing the Right Retirement Plan as a Self-Employed Entrepreneur

If you're self-employed, selecting between a Solo 401(k) and a SEP IRA is one of the most impactful financial decisions you can make. Both plans offer significant tax advantages, high contribution limits, and the ability to supercharge your retirement savings. However, they function very differently, and your choice can mean thousands of dollars in tax savings or missed opportunities.

In this comprehensive guide, we’ll explore the key differences, updated 2025 contribution limits, tax-saving strategies, and real-world scenarios to help you make the best decision for your financial future.

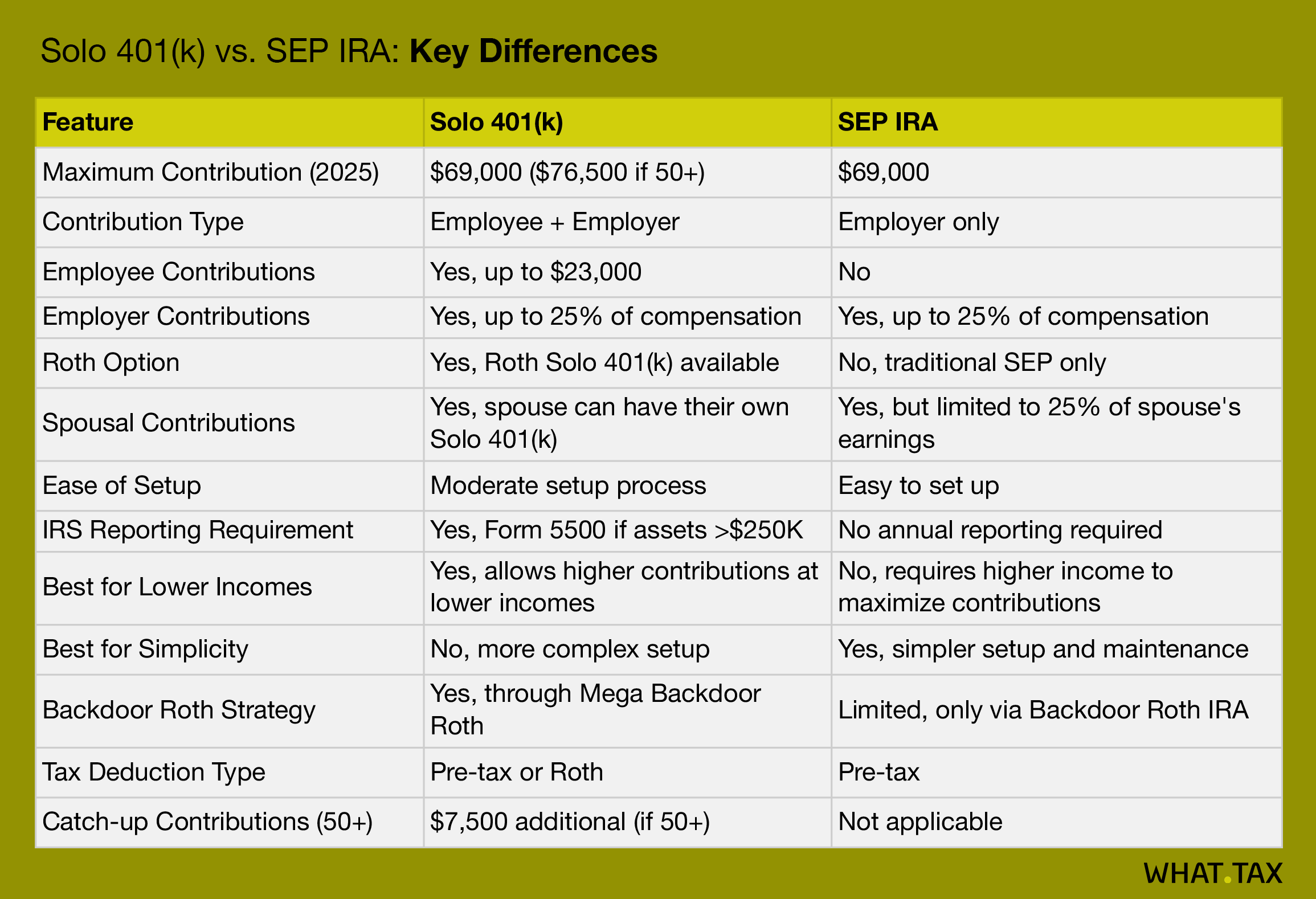

1. Maximum Contribution Limits for 2025: How Much Can You Save?

One of the biggest reasons business owners choose Solo 401(k) or SEP IRA plans is the ability to contribute significantly more than a traditional IRA or Roth IRA.

Solo 401(k) (2025 limits): Up to $69,000 ($76,500 if age 50+ with catch-up contributions)

SEP IRA (2025 limits): Up to 25% of net earnings, capped at $69,000

Key Difference: Contributions at Lower Income Levels

The Solo 401(k) is superior if you have a lower net income, as it allows you to contribute as both an employee and an employer.

Example: If you earn $100,000 from your business:

SEP IRA: You can contribute 25% of your net earnings → $25,000.

Solo 401(k): You can contribute $23,000 as an employee (2025 limit) + 25% of earnings as an employer (another $25,000) → Total: $48,000.

✔ Winner: Solo 401(k) if your income is below $275,000 since it allows you to reach the maximum contribution faster. ✔ SEP IRA works well for those earning over $300,000, where the 25% rule allows maxing out the contribution without additional calculations.

2. Roth Options & Backdoor Strategies

Solo 401(k) = Roth Potential Up to $69,000

A huge advantage of the Solo 401(k) is the ability to contribute directly to a Roth 401(k)—meaning tax-free withdrawals in retirement. The SEP-IRA does not allow Roth contributions.

If you earn $150,000, you can contribute $23,000 to your Roth Solo 401(k) (2025 limit) and the employer portion to traditional pre-tax.

Additionally, you can contribute after-tax dollars beyond the employer limit and do an in-plan Roth conversion, creating a mega backdoor Roth opportunity!

SEP IRA = Backdoor Roth Only via IRA

Since the SEP IRA is strictly pre-tax, the only Roth conversion strategy is through a Backdoor Roth IRA, which is limited to $7,000 in 2025 ($8,000 if you are 50+).

✔ Winner: Solo 401(k) for those who want tax-free Roth savings.

3. Spousal Contributions: How to Double Your Retirement Savings

If you have a spouse working in your business, you can effectively double your tax benefits.

Solo 401(k) allows each spouse to have their plan, doubling the contribution limits (up to $138,000 total in 2025!).

SEP IRA also allows spousal contributions, but each spouse’s contribution is limited to 25% of their compensation.

✔ Winner: Solo 401(k) if you have a spouse and want maximum contributions.

4. Ease of Setup & Maintenance: Which One is Simpler?

Many entrepreneurs prefer a retirement plan that requires less paperwork and fewer IRS reporting obligations.

Solo 401(k): More complex to set up and requires Form 5500 if assets exceed $250,000.

SEP IRA: Easier to establish, no annual filings, and simple employer-only contributions.

✔ Winner: SEP IRA if you want the simplest option.

5. Contribution Timing: When Do You Need to Fund the Plan?

Solo 401(k): Employee contributions must be made by December 31st of the tax year, but employer contributions can be made until your tax filing deadline (including extensions).

SEP IRA: All contributions can be made until the tax filing deadline, including extensions.

✔ Winner: SEP IRA offers more flexibility for tax planning.

6. Which Plan Saves You the Most in Taxes?

If you are a high earner looking for maximum tax deductions, the Solo 401(k) wins in almost every case because it allows you to contribute at lower income levels and offers Roth advantages.

Breakdown by Income Level

Under $150,000 → Solo 401(k) allows for much higher contributions.

$150,000 - $275,000 → Solo 401(k) wins for Roth and maxing out earlier.

Above $300,000 → SEP IRA is simpler and works just as well if you don’t need Roth options.

Final Verdict: Which One Should You Choose?

✔ Solo 401(k): Best for maximizing contributions, utilizing Roth options, and optimizing tax savings. ✔ SEP IRA: Ideal for those seeking simplicity, ease of setup, and fewer compliance requirements.

✔ Overall, the Solo 401(k) is the best option for most self-employed entrepreneurs because it allows for more contributions, better tax flexibility, and Roth opportunities.

However, the SEP IRA is a strong, low-maintenance option if you prioritize simplicity and don’t want the extra paperwork.

Next Steps: Take Action Now

If you want a Solo 401(k), check out providers like Fidelity, Schwab, or Vanguard.

If you prefer a SEP IRA, you can set one up quickly with most brokerage firms.

By making the right choice today, you can save thousands in taxes and build a secure financial future. 💰