Make Idle Cash Work Harder

How to turn every sleepy dollar in your operating account into a compounding engine, before Congress slams the door

The Cash-Drag Epidemic

Most owners think of cash as “safe.” Yet the data scream otherwise:

The median U.S. small business keeps only 27 days of outflows in reserve, and that figure hasn’t budged since the pandemic. (For Small Businesses: Cash is King | JPMorganChase)

The typical business checking account still pays 0.05 % APY. Parking $1 million there earns a laughable $500 yearly before tax. Contrast that with today’s online savings accounts that top 4 %, or Treasury bills north of 4 %. (CIT Bank Platinum Savings Account, Announcements, Data & Results - TreasuryDirect)

Thought experiment: At a 37 % marginal rate, you delay moving $1 million from 0.05 % to 4 %, “bleeds” roughly $720 in opportunity cost every week. Extend that over a 52-week fiscal year, and the silent leak tops $ 37k—enough to bankroll an entry-level hire.

2025 is a gold-plated window to reverse the leak because three forces converge:

Bigger retirement buckets under SECURE 2.0.

The last meaningful year of 40 % bonus depreciation before it plummets to 20 % in 2026.

Expanded credits and deductions from the Inflation Reduction Act.

Below is the field manual. You can pick the moves that fit your runway and appetite; please ignore the rest. Just do nothing.

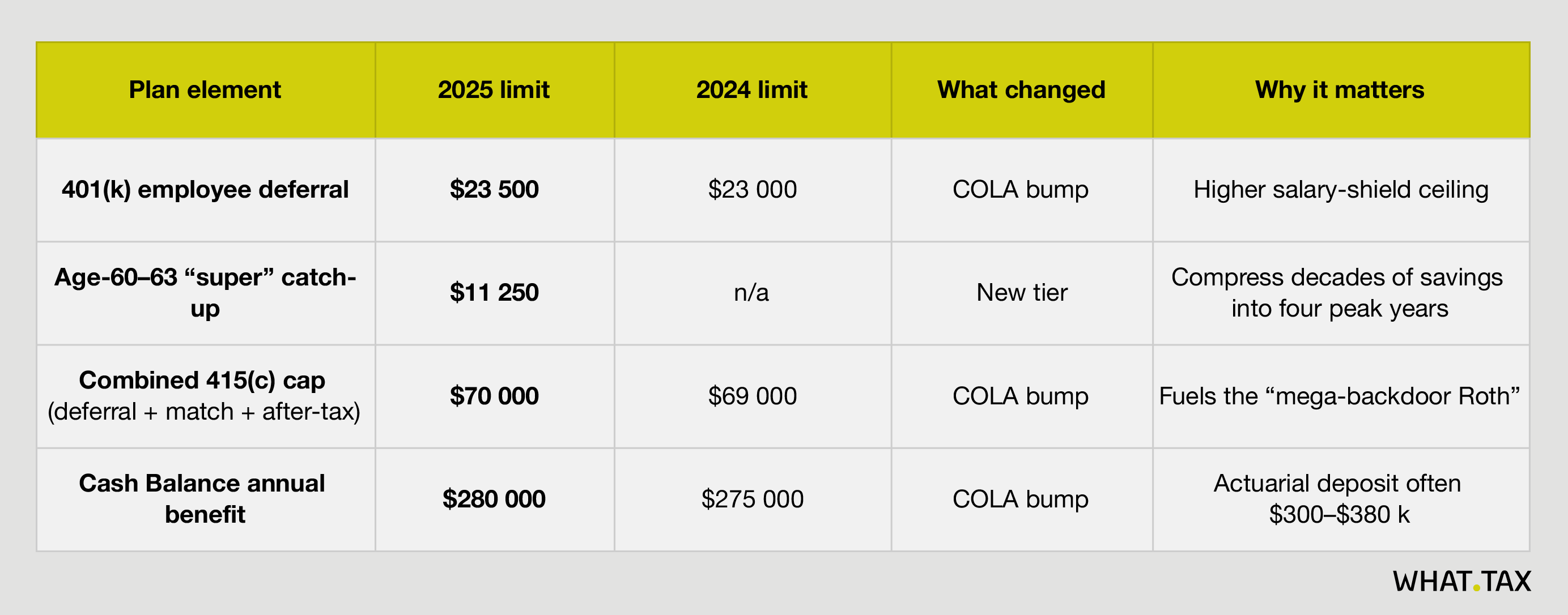

1. Build a “Retirement Stack” That Shelters $ 451,000+ per Owner

SECURE 2.0 juiced almost every dollar limit for 2025:

Sources: IRS Notice 2024-80, COLA tables. (IRS, COLA)

How the stack plays out

Profile: 52-year-old founder, $ 200k W-2, high-margin SaaS.

401(k) ↳ Defers $23 500 + $7 500 standard catch-up.

After-tax 401(k) ↳ Company kicks in $ 39,000, immediately converted to Roth (mega-backdoor).

Cash Balance Plan ↳ Actuary funds $ 275,000.

Total shelter: $ 345,000 → $ 127,650 federal tax saved at 37 %. The after-tax portion now compounds tax-free for life, while the pre-tax nest egg turbo-charges retirement funding.

Implementation tip: Combine a safe-harbor match (3 % non-discretionary or 4 % enhanced) with an “integrated” profit-sharing formula for top-heavy compliance—then pour everything else in after-tax.