Getting Paid as an S-Corp Owner: The Smart Way to Do It

How to Slash $25k+ in Taxes Annually with Updated 2025 Strategies

Hello, Dear Friends!

Taxes can be complex, but a smart approach can make all the difference. In this concise guide, we’ll explore why an S-Corp remains one of the best tools for preserving your hard-earned money. Get ready to discover practical insights for reducing taxes and keeping more of what you earn.

The S-Corporation remains the most powerful tax-optimization structure for American entrepreneurs with net earnings of $60,000 or more. Nevertheless, a staggering majority—over 80%—of business owners continue to over-contribute to federal coffers by mismanaging the balance between wages and shareholder distributions. Going into 2025, with inflationary pressures and heightened IRS scrutiny, properly calibrating this balance is non-negotiable.

A meticulously planned S-Corp structure allows you to preserve approximately $0.153 of every dollar that self-employment taxes might otherwise swallow. Here’s how to ethically and effectively capitalize on these savings.

Why 2025 Demands S-Corp Optimization

The IRS amassed roughly $1.4 trillion in payroll taxes in 2023. By intelligently positioning income as part salary (W-2) and part shareholder distribution (K-1), S-Corp owners can legitimately circumvent up to 59% of these levies.

Key Adjustments for 2025:

Social Security Wage Base: $175,000 (a 4.8% increment from 2024)

Medicare Surcharge: An additional 0.9% on salaries surpassing $200,000 for single filers or $250,000 for joint filers

Evolving State Regulations: 13 states now impose surcharges or franchise taxes on S-Corp pass-through revenue (e.g., California’s 1.5% franchise tax)

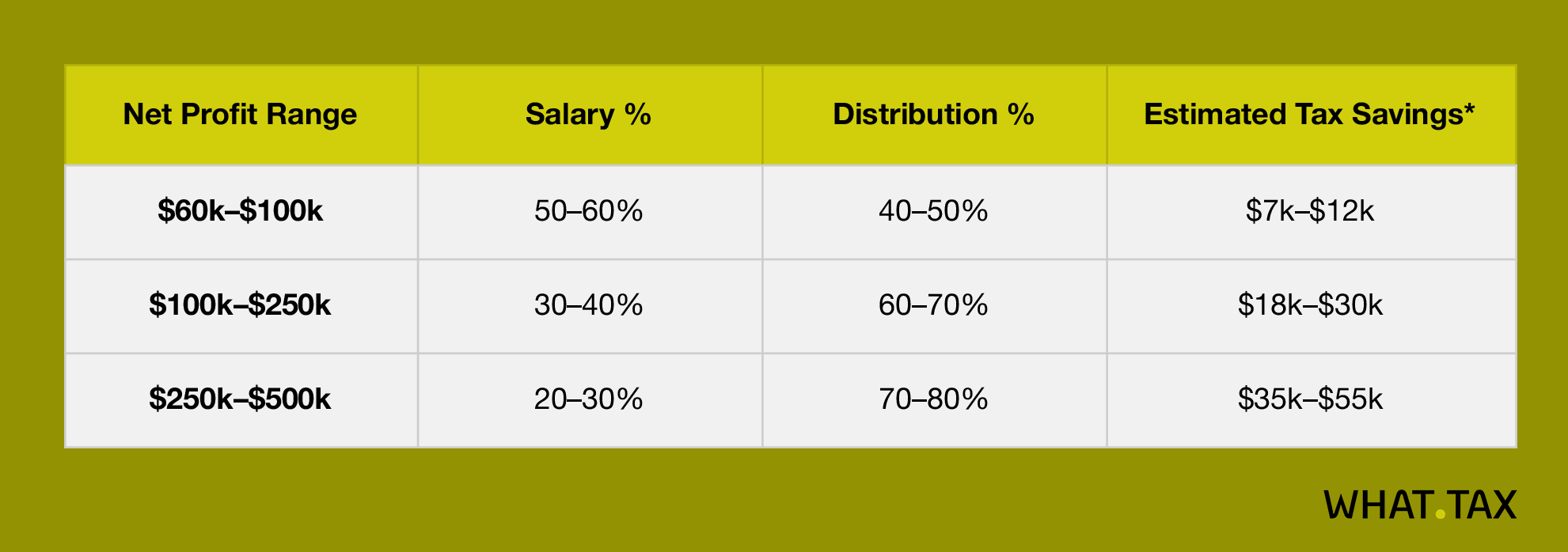

The 2025 Salary-Distribution Matrix: A Tactical Framework

IRS guidelines mandate that shareholder-employee compensation aligns with “reasonable compensation” benchmarks. Meanwhile, distributions avoid the 15.3% self-employment tax. The matrix below offers a calibrated approach for 2025:

If a consultant earns $300,000 in net profit:

Salary: $70,000 (≈23.3%)

Distribution: $230,000 (≈76.7%)

Resulting Tax Savings: $230,000 × 15.3% = $35,190

Ensuring Reasonable Compensation in 2025: Staying IRS-Compliant

Roughly 2.5% of S-Corporations face annual IRS audits. The following factors guide whether your salary passes “reasonable compensation” scrutiny:

Industry Benchmarks: Leverage reputable data (e.g., Payscale, Bureau of Labor Statistics) to substantiate salary levels.

Profitability Metrics: High net profit does not inherently necessitate a proportionally high salary.

Dividend Ratio: Keep distributions within approximately three times the salary. For instance, a $70k salary ordinarily supports up to a $210k distribution.

Nature of Duties: Active executives and owners commanding the bulk of managerial or operational tasks warrant proportionally higher wages.

Pro Tip: Integrate 2025-specific compensation surveys based on geographic location to bolster your case. For instance, a Phoenix-based digital marketing agency owner might reasonably draw $65k, whereas a New York City SaaS founder may need $150k to align with industry norms.

Sophisticated 2025 Strategies to Amplify Tax Efficiency

1. Solo 401(k) Integration

Employee Contributions: Up to $23,000 from salary

Employer Profit-Sharing: Contribute 25% of the W-2 wage (capped to reach a possible aggregate limit of $69k)

Net Benefit: Significantly reduce taxable income while accumulating retirement wealth.

2. Health Insurance Premium Deductions

Premiums paid through the S-Corp remain 100% deductible, circumventing the usual 7.5% AGI threshold.

Combine with a Health Savings Account (HSA) for a triple-layered tax advantage (pre-tax contributions, tax-free growth, and tax-free withdrawals for medical expenses).

3. Navigating State-Specific Nuances

Texas/Florida: Zero state income tax incentivizes more aggressive profit distribution.

California: Offset the 1.5% franchise tax by deducting it at the federal level, preserving more capital overall.

Consequences of Mismanagement

Faltering in S-Corp compliance can trigger three major pitfalls:

Reclassification Risk: The IRS may retroactively reclassify distributions as wages, imposing hefty back-taxes and associated penalties.

Underpayment Penalties: Delayed or inadequate payroll tax remittances incur fines up to 10%.

Worker Misclassification: Overusing independent contractors instead of W-2 employees invites audits and severe sanctions.

Mitigating Measures: To automate tax filings, opt for robust payroll solutions (e.g., Gusto, Rippling). Budget $1,200–$2,500 annually for S-Corp administrative responsibilities, including tax preparation and payroll services.

Case Study: Transitioning from LLC to S-Corp in 2025

Consider Sarah, a freelance software developer who reevaluated her structure upon surpassing $150k in net earnings:

Former LLC Setup: $150k × 15.3% = $22,950 (self-employment tax)

New S-Corp Paradigm:

W-2 Salary: $60k → $9,180 (payroll tax portion)

K-1 Distribution: $90k → $0 (no self-employment tax)

Total Savings: $22,950 – $9,180 = $13,770

Net Savings (After S-Corp Costs): $13,770 – $1,800 (S-Corp fees) = $11,970

2025 Action Plan: Elevate Your Tax Strategy

Crunch the Numbers: Once your net profit exceeds $60,000, evaluate the S-Corp transition.

Implement Strategic Payroll: Refer to the aforementioned matrix and ensure distributions do not exceed 80% of total net profit.

Maintain Comprehensive Documentation: Retain corporate minutes, justifications for salary levels, and profit-sharing records.

A Word of Caution: IRS enforcement now employs AI-driven analytics. Collaborate with a CPA who specializes in S-Corporations; relying on generalist tax preparers could cost you tens of thousands of dollars annually.

The S-Corp remains a formidable instrument for safeguarding wealth. In 2025, it holds the potential to retain over $25,000 of your hard-earned capital each year. Harness its advantages, fortify your compliance, and reap the lasting rewards of a well-executed tax strategy.